It’s fair to say that the banking stocks are the backbone of stock market. Currently there are 9 banking stocks I Nifty 50, contributing 18.56% weightage to Nifty 50. Mutual funds have their maximum investment in banking stocks. Moreover according to experts revival of Indian economy is not possible without the participation of backing sector. These are the 5 undervalued stocks from the Bank Nifty with extremely strong fundamentals, having the potential to give good returns in the long run

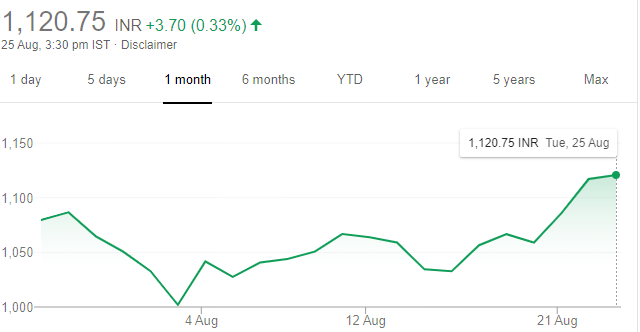

HDFC Bank Limited (NSE: HDFCBANK)

Strong quarter; not much affected by the pandemic

Incorporated in August 1994, HDFC Bank provides corporate banking and custodial services and is also involved in treasury and capital markets. In addition, it offers project advisory services and capital market products, including GDR and currency bonds.

- During Q1FY21, loans and advances grew 20.9% YoY, while deposits grew by 24.6% YOY. Operating profit before provisions increased by 15.2% YOY to Rs 12,829 crore.

- Capital Adequacy Ratio increased to 18.9% from 16.9% in Q1FY20.

- GNPA/NNPA ratio stood at 1.36%/0.33% during the quarter.

- HDFC Bank continues to deliver strong results even in tough times. Buy the stock with a target price of Rs. 1,403.

Better than anticipated growth across top-line and bottom-line

Q1FY21 Net interest income rose 17.8% YoY to Rs. 15,665cr, backed by further strong growth in loans and advances amounting to Rs.1003299 crore. On the other hand, customer deposits also grew by 24.6% YoY to Rs. 1,189,387cr, with time deposits witnessing a 23.7% YoY growth, and CASA growing by 26.0% YoY. The bank’s contribution from other income was impacted by the slowdown in economic activity as there was a decline in retail loan origination, sale of third party products. Nonetheless, this was partly offset by the reduction in operating expenses, as cost to income ratio stood at 35% compared to 39.5% in the same quarter last year. PAT grew by 19.6% YOY to Rs 6,659 crore despite a substantial gain in provisions +Rs 3,892cr, +48.9% YoY) this quarter.

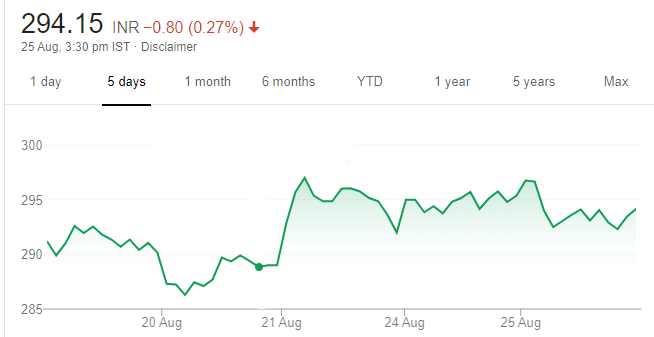

ICICI Bank Limited (NSE: ICICIBANK)

Incorporated in the year 1994, ICICIBank is a banking company with a market cap of Rs 223971.78 Crore.

For the quarter ended 30-06-2020, the company reported a Consolidated Interest Income of Rs 15335.70 Crore, down -2.20 % from last quarter Interest Income of Rs 15681.08 Crore. The bank reported net profit after tax of Rs 3586.91 Crore in latest quarter. Deposits grew by 21.3% YoY and 4% QoQ. Growth in CA deposits stood at 19% YoY (down 6% QoQ) while SA deposits grew by 12% YoY (flat QoQ). The average CASA ratio declined from 42.3% in 4QFY20 to 41% in 1QFY21. Asset quality metrics showed improvement with GNPA/NNPA ratio declining by 7bps/18bps QoQ. PCR improved to 78.6%, one of the strongest in the banking sector. At the current juncture, we keep our NPA estimates unchanged as the ultimate slippage from the moratorium book still remains largely unclear. Though what is encouraging is the reduction in moratorium numbers as well as bank’s proactive approach in strengthening the balance sheet by providing for the unanticipated stress. We think IBL’s retail loan book construct (~50% mortgages). On the valuation front, the standalone bank is trading at 1.2x FY22E ABV. We think that besides the standalone entity, the subsidiaries have immense growth opportunities in their respective industries given the broad financialization theme and are overall franchise value enhancers from a broader viewpoint.

Investment Ratings

The month of April and May was severely impacted by nation-wide lockdown which also led to slower growth in advances. High provisioning owing to COVID-19 has put downward pressure on the bank’s bottom line. Still, we expect the growth momentum to resume from late FY21 as the bank’s balance sheet remains strong.

Indusind Bank

Careful on lending, concentrating on balance sheet granularity

IndusInd Bank (IIB) reported operating profit growth of 13% YoY and 2.5% QoQ on the back of 16.4% YoY and 2.5% QoQ growth in NII and decline in open (down 1% YoY, 11.4% QoQ) even as the loan book contracted by 4.2% QoQ. On a YoY basis, the loan book grew by 2.4%. The strong NII growth came on the back of a healthy NIM of 4.28%, which expanded by 23bps YoY and 3bps. This is despite the fact that the balance sheet liquidity increased significantly. Deposit inflows were good as indicated by 5.3% QoQ growth, though the focus remained on accreting granular retail deposits by offering a higher rate. Going forward, the strategy is to improve balance sheet granularity. In line with this, the bank shed some high-rate corporate deposits during the quarter. The cost of deposits fell to 5.73% from 6.05% in 4QFY20, which also helped to some extent in margin expansion. Provisions remained high at Rs22.6bn, with the objective being to increase the PCR by

~400bps QoQ to 67% along with creating contingent provisions to cushion the COVID-19 asset quality impact. Total slippages stood at Rs15.4bn, 80% of which were corporate in nature. Slippages from the three stressed groups, a coffee group, and a healthcare provider amounted to Rs10.9bn. As per the bank, NPA recognition in the corporate segment was in line with its prudent and more conservative asset recognition approach. GNPA ratio increased from 2.45% in 4QFY20 to 2.53% in 1QFY21 while the NNPA ratio was down 5bps QoQ at 0.86%. The absolute level of GNPAwas down by nearly 1%. More importantly, the loan book under moratorium is 16%. For the corporate segment, the book under moratorium is 9% while that in the consumer segment it is 19%. Collection trends in the consumer finance portfolio seem to be improving. More than 90% of the book under moratorium is secured.

IDFC First Bank

Moving in the right direction

IDFC First delivered a strong performance despite a challenging environment. Except moratorium in phase2 still high at 28%, the bank recorded an improvement on all parameters. The bank offered Morat 2 to 28% of its customers by value. 35% is in the wholesale financing portfolio and almost 23% is in retail assets incorporating rural portfolio. Provision was at | 764 crore, including | 375 crore related to Covid-19 over and above | 225 crore done in Q4FY21. Asset quality witnessed a strong sequential improvement with the GNPA &NNPA ratio improving ~61 bps and ~43 bps to 1.99% and 0.51%, respectively. Gross NPA of the retail loan book was at 0.87% vs. 1.77% as of March 31, 2020, and the net NPA percentage of the retail loan book of the bank was at 0.24%. PCR has been improving in the last five quarters and has reached 74.93% from 64.53% in Q4FY20.NII grew 38% YoY to | 1,626 crore, up from | 1,174 crore. NIM rose to 4.53% in Q1FY21 from 3.01% in Q1FY20, up 4.24% QoQ. Funded assets fell QoQ to | 104050 crore from | 107400 crore. Within the same, wholesale book, as targeted, de-grew ~6.3% QoQ to | 37928 crore. The retail book grew 26% YoY but marginally fell QoQ at | 56043 crore. CASA accretion remained robust growing 145% YoY & CASA reached 33.7%.PAT for Q1FY21 was at | 94 crore as compared to a loss of | 617 crore for Q1FY20 and profit of | 72 crore in Q4FY20, up 31% (QoQ). Cost to income ratio (excluding trading gains): 68.72% for Q1FY21.The bank has raised | 2000 crore via preferential share route at| 23.19/share. CRAR was at 15.03%, while the CET1 ratio was at 14.53%.

Bandhan Bank

Standardized performance post-mergerBandhan Bank operates as a commercial bank that provides checking accounts, savings deposits and money market, mortgage and term loan services. It also offers card facilities and internet banking services. Bandhan bank merged with Gruh finance on 17th October, 2019.

- Loans and advances increased by 83.9% YoY in Q3FY20, while the contribution of micro banking declined to 61.0% after the merger.

- Bank’s deposit grew 58.5% YoY with CASA up 31.4% YoY in Q3FY20.

- Net interest margin (NIM) declined 260bps YoY to 7.9%, due to a decline in Yield on advances and an increase in the Cost of funds.

- GNPA/NNPA ratio stood at 1.93%/0.81% in Q3FY20 (vs 1.76%/0.56% in Q2FY20).

- We expect the potential synergies from the merger and wider customer base will fuel growth.

Earnings rose amid a change in corporate tax rate yield on advances declined 140bps YoY to 14.0% (vs. 15.4% in Q3FY20) and cost of funds increased 90bps YoY to 7.2% (vs. 6.3% in Q3FY20) resulting in a decline of Net interest margin by 260bps to 7.9% in Q3FY20. Net interest income increased by 37.0% YoY to Rs. 1,540cr in Q3FY20, thereby leading pre-provision profit to grow 40.4% YoY to Rs. 1,264cr. As the bank benefitted from the merger with Gruh Finance, Net income grew 120.7% YoY to Rs. 731cr, also fuelled by a decrease in the corporate tax rate.

Important points

- Total banking outlets grew to 4,288 including 195 Gruh.

- The bank has created an additional provision of Rs. 2bn for the stressed MFI books in certain areas of northeastern states.