FM ordered banks to approve credit to micro, small, and medium enterprises (MSMEs) covered under emergency credit facilities. Banks have sanctioned Rs 1.3 trillion to MSMEs under this scheme as of July 23. Of that, Rs 82,065 crore has been disbursed.

The decision of the Government of India in regards to Business & Finance:

Corona has spread around the world like wildfire and we have all been locked down to avoid the burn and break the chain of the virus. The Government of India has been taking appropriate steps to alleviate the sufferings of the citizens.

On 29th July 2020, Hon’ Prime Minister Narendra Modi told bank officials that small and medium enterprises (SMEs) i.e. small scale businesses should be allowed to look into loans for new investment. The loan seeking business-men/women should not be dismissed even if the previous loan has not been repaid.

On 29th July 2020, Hon’ Prime Minister Narendra Modi told bank officials that small and medium enterprises (SMEs) i.e. small scale businesses should be allowed to look into loans for new investment. The loan seeking business-men/women should not be dismissed even if the previous loan has not been repaid.

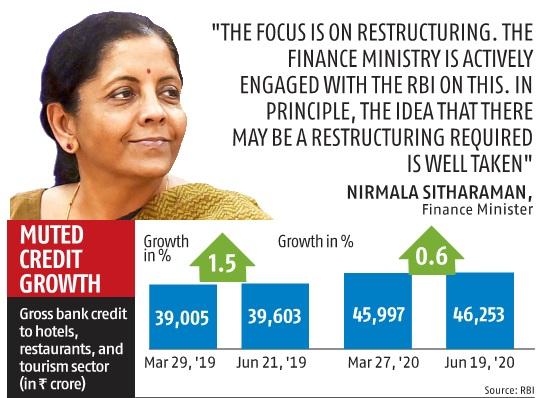

Showing a glimmer of hope to industries, on 1st August 2020, Finance Minister Nirmala Sitharaman said that the bank should not reject the loan applications of small and medium enterprises. If these loan seekers qualify for borrowing, then they should be sanctioned lending.

To cope with the shock of the lockdown, the Modi government has set up a guarantee fund for emergency loans. Despite that, the finance minister warned the bank officials that the loans were not being delivered to what they promised, “I will look into it myself”, she said.

Bank official’s take on the expansion of loan credit:

Although the industrialists are happy with the assurance of the finance minister, the bank officials are worried. Their fear is that on the one hand, generous loan disbursement, on the other hand, to make the loan repayment instalments easier, non-performing loans or NPAs may increase. The Reserve Bank has already expressed fears that the NPA rate could reach 12.5% in March 2021. Which was 8.5% in March this year.

What the banks say about the impact?

According to the bank officials, if the conditions for repaying the loan are made easier in all cases, it will be misused. A similar approach was taken in 2008 after the global financial crisis. The unpaid debt is hidden under the carpet. Many banks provide new loans to reduce the burden of NPAs in the account-pen, so that corporates can repay previous loans with that money. But new loans also remain unpaid. In 2015, all came under the direction of the Reserve Bank.

Bankers are against extending the moratorium period. For instance, HDFC Chairman Deepak Parekh recently urged RBI Governor Shaktikanta Das not to do it. Parekh said many entities capable of repaying were taking advantage of the scheme and this was hurting the financial sector, especially non-banking.

Bankers are against extending the moratorium period. For instance, HDFC Chairman Deepak Parekh recently urged RBI Governor Shaktikanta Das not to do it. Parekh said many entities capable of repaying were taking advantage of the scheme and this was hurting the financial sector, especially non-banking.

Finance Minister’s assurance to Banks:

The finance ministry, however, thinks that the economy will start again if a one-time solution is given to the companies that are unable to repay their loans due to the shutdown. In the case of housing, work can start again only if some additional capital is found. But bank officials fear that new loans will be added to previous unpaid loans. After discussions between the officials of the Ministry of Finance and the Reserve Bank, the officials of the two sides think that a solution can be arranged for some areas and not for all.

RBI governor recently saying that industry had to find new ways to fund infrastructure projects because banks, struggling with bad loans, would not be able to give them money. The finance minister emphasised reciprocity in trading arrangements with countries to which India has opened up.

What was the Loan Moratorium offered by RBI?

Considering the economic consequence of the Corona virus pandemic, RBI granted a deferment period of three months for EMI payments. This facility was granted from the months of March to May 2020. However, at present the RBI Has extended it till the end of August i.e. 6 months of extension period in total.

What is a Moratorium period in relation to EMIs & Loans in simple terms?

A moratorium period is a time during the loan term when the borrower is not required to make any repayment. It is a waiting period before which repayment by way of EMIs begins. Normally, the repayment begins after the loan is disbursed and the payments have to be made each month. However due to this moratorium period, the payment starts after some time.

Education loans provide this feature. This is because education loans are repaid by the students after they start earning and build their finances.

During the moratorium period the bank will calculate interest on your loan on simple interest basis. Interest calculations will start as and when amounts are disbursed to you and not on the entire loan amount at once.

This interest will be accumulated until the end of the moratorium period. There are some banks that offer a concessional interest rate if you take the loan and arrange to pay the interest portion of the loan during the moratorium period.

Simple example: if a loan amount of Rs 1 lakh is released at the start and interest rate is 11% per annum, a total interest of Rs 11,000 per annum or Rs 33,000 for a three-year moratorium period will be accumulated.

Struggling to get A Business Loan in India?

The federal government in India was urging small and medium-sized businesses (MSMEs) to shed self-doubt and unleash their “animal spirits” until just six months ago. The sudden coronavirus pandemic not only knocked revenues off MSMEs’ balance sheets, but also affected their hopes of survival.

In a bid to rescue MSMEs from defaults, the government offered relief in the form of collateral-free loans, subordinate debts and equity infusion through its Fund of Funds scheme, which proposes to buy up to 15% growth capital in high-credit MSMEs.

Earlier this week, India’s Finance Minister Nirmala Sitharam confirmed banks had sanctioned INR 1.27 lakh crore loans to MSMEs of the INR 3 lakh crore ($39 billion) announced in May. This figure is the collective loan that India’s 12 public sector banks, 22 private sector banks and 21 non-banking financial companies (NBFCs) have committed to grant.

That means more than half the capital the government has promised to lend is still available to businesses.

How to apply for MSME loan from Banks?

An easy way of getting a MSME loan from a bank is by applying for a loan via the website. This is the only government portal for MSME registration.

An easy way of getting a MSME loan from a bank is by applying for a loan via the website. This is the only government portal for MSME registration.

Since the government announced a change in the definition of MSMEs in May, all MSMEs have to register on this website to create an Udyam Registration Number. This number is linked to the MSME owner’s Aadhaar and PAN Cards, both of which help banks validate a person’s bank account details, residential address and their financial stability along with technical details such as telephone numbers which will receive unique codes to validate loan requests and subsequent disbursal.

Banks will be able to retrieve all the information required to grant a quick loan to the MSME whose Udyam Registration Number is available.

Impact on the Economy of our nation?

Increase of debt acquisition is one of the main concerns which our economy will face. Rating agencies have forecasted warnings of storms in the form of debt deferrals. This going to affect our credit flow and the economy to a deep extent. However due to assurance from the Central bank of India and the Ministry of finance. The outcomes can only be waited for in the future depending on the appropriate authorisation and correct implementation of these schemes for the actual small businesses of India.

The government had proposed to provide support of up to Rs 3 lakh crore to small businesses and SMEs as an aid for them to meet the impact of Covid-19 financial loss amplified by lockdown. This might also help pay rent and salaries. However as of 23th July 2020, Rs 1.3 lakh crore has been sanctioned by public and private sector lenders, with disbursement estimated at Rs 82,000 crore and above.

As international trade faces questions from the global lockdown and other international wars, the minister said that reciprocal arrangements are being asked with the countries with which India has opened up its markets. She added that reciprocity is a very critical point in India’s trade negotiations.

Meanwhile, earlier this week, FM Sitharaman had said that the government is working on completing the stake sale process of about 23 PSU companies whose divestment has already been cleared by the Cabinet. She had also assured that she would soon meet small finance firms and non-banking finance companies (NBFCs) to review the credit being extended by them to businesses.

Meanwhile, earlier this week, FM Sitharaman had said that the government is working on completing the stake sale process of about 23 PSU companies whose divestment has already been cleared by the Cabinet. She had also assured that she would soon meet small finance firms and non-banking finance companies (NBFCs) to review the credit being extended by them to businesses.

Encouraging the Atma-Nirbhar Bharat mission and highlighting the government’s step to open up all sectors for private firms, Nirmala Sitharaman had said that the final call as to which are the strategic sectors is not made yet.