The issue of non-performing assets in the Indian banking sector has received a lot of media attention in public discussion. A large number of these bad loans were originated in the period 2006 to 2008 when economy growth was strong.

In previous infrastructure projects such as power plants, sugar, mills, etc. Had been completed on time and within budget it was a period in which the world economy as well as the Indian economy were booming.

Indian forms borrowed furiously in order to avail the growth opportunities they saw coming. Most of the investment went into infrastructure and related areas- telecom, power, roads, aviation, steel, etc.

Businessmen were overcome with exuberance partly rational and partly irrational they believe as many other state that India had entered into an era of 9% growth during this time.

Banks also made the error of assuming past growth and performance for the longer term . They were willing to fund higher debt in projects with little promoter money. A lot of times banks didn’t even do their own due diligence and analysis.

Instead they just relied on projection reports of businessman. Banks were chasing corporates with open cheque-books asking them who named the loan amount they wanted. This was a classic case of irrational exuberance.

Unfortunately, growth doesn’t always happen needless to say . The years of strong global growth before the 2008 financial crisis were followed by a slowdown which impacted India as well those projects which assumed strong demand. Projections now became increasingly unrealistic as domestic demand slowed down. During this time, governance issues cropped up.

In Indian government various scams came to light which induced fear of investigation among government bureaucracy. This reduced decision-making in Delhi contributed towards project delays.

Thanks to problems in acquiring land and getting environmental clearances. Several projects got stuck. Cost overruns escalated for stalled projects and they became increasingly unable to service debt as for motifs equity declined in the projects.

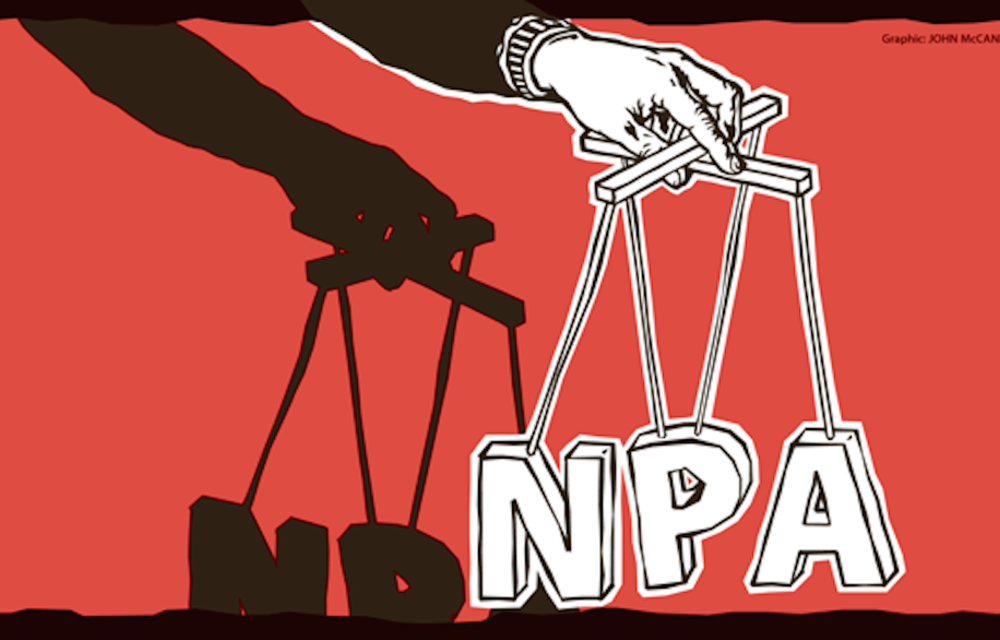

They lost interest ideally. These projects should have been taken over by banks and that should have been restructured at this juncture. Promoters needed to either bring more money in the project lose ownership. Unfortunately, this didn’t happen due to lack of a bankruptcy code. At the time in India without bankruptcy code bankers had little tools to threaten promoters.

Lawsuits in India are notoriously long and tedious. They dragged on for years and promoters took advantage of these loopholes writing off the debt by bankers would have simply been a gift to these promoters and additionally it would have invited the attention of investigative agencies. So bankers simply kept these stuck projects as zombie projects in their books neither dead nor alive.

Generally, loans to large infrastructure projects are given by a combination of multiple banks to reduce risk. However, once these projects get stuck and these loans became unserviceable promoters simply played one bank against another. It was in everyone’s interest to extend the loan by making additional loans so that promoter can pay interest and pretend it was not a bad debt.

It solved two problems- one promoters didn’t have to bring in more money and second bankers didn’t need to restructure the debt and show losses in their annual reports. In reality though since these loans were bad bank’s profitability was just an illusion and losses on their balance sheets were ballooning.

It was a ticking time bomb. Unless these stuck projects somehow miraculously recovered on their own these loans were going to blow up one day in a big way.

These deceptive accounting by Indian banks were only postponing.

The Domesday behind this huge NVA problem were a combination of factors banker exuberance incompetence and corruption bankers were overconfident while giving loans during boom period.

And they did very little independent analysis of the project cash flows unscrupulous promoters poured oil in the fire by inflating the cost of machinery and equipment wire / invoicing the bills and simply bad intent a portion of this NPA was due to outright fraud.

But major portion was due to lack of decision-making and undo delays on the part of bureaucracy which made large projects unviable and increase their costs. Although the size of frauds relative to the total volume of NPA is relatively small. These frauds have been increasing and there have been no instances of high-profile fraudsters being finalized.

This NPA bubble was busted during the tenure of RBI governor Raghuram Rajan. He constituted a committee for asset quality check of Indian banks and made them disclose all the loans which were behind their payment schedule.

He realized the inefficient loan recovery system gave promoters tremendous power over lenders and that they were just exploiting the system. During this time at RBI there were several changes made in the debt recovery tribunal and SARFAESI act to give Indian bankers more power to seize the assets of promoters and auction them off to recover some costs.

However, you can understand the enormity of NPA problem in Indian banks. By the fact that currently close to 10 percent of all bank loans in INDIA are NPA provisional estimates suggest that the total volume of gross NPA in the economy stands more than 10 lakh crore or 150 billion dollars about 85 percent of these in PS are from public sector banks.

For instance, NPS in the State Bank of India are more than 2 lakh crore or 30 billion dollars. this huge NPA puts burden on the banks’ ability to start out fresh credit cycle within the economy. Indian economy needs strong banks who can finance large public projects like roads, bridges, hospitals, etc. due to unavailability of large capital.

The GDP growth had been hurt in the past 5 years India has tremendous infrastructure deficit and undertaking these projects alone can generate millions of jobs and contribute towards higher GDP growth rate.

However, this NPA problem will still take years to fully resolve as most NPA cases are taking years to complete 701 cases have been registered so far and only 176 cases have been resolved as of March 2018 under the insolvency in bankruptcy court.

Public sector banks had been the worst hit due to this crisis as they accounted for a lion’s share of the toxic loans. The condition was so alarming that at one point the banking regulator RBI had to put 12 Indian banks under a corrective action framework where they had to face strict operational restriction while one of them was even barred from lending.

Banks have witnessed a decline in their profitability in the last few years making them vulnerable to adverse economic shocks and consequently putting consumer deposits at risk.

Tax we can tell you is only one part of the problem, the other is debt. The focus is on recovery and enforcement. Big businesses do not want to repay loans. They want refinance without accountability.

When dubious measures fail they blame the government of being anti-business but strict measures must be enforced NPAs or non-performing assets are bleeding in India today.

Banks are under a mountain of debt. Here’s a quick look at India’s NPA story life was good in the mid-2000s but so it seemed booming growth strong outlook banking lending to business on extrapolation of growth and outlook and then came the 2008 global financial crisis.

It was felt in India to businesses could not repay interest on the loans growth stagnated banks under fire businesses under financial stress. The twin balance sheet problem came into being the reserve bank acted.

It tried various ways to restructure debt recovery. tribunals were set up SARFAESI Act of 2002 made recovery process easier but recovery was low. The RBI created a large loan database with the updated status of the loan.

This was a landmark move to help identify. The extent of pain and India’s banking sector here’s the extent of bad loans as of March 2018 gross NPA’s in India’s public sector banks alone was 8.95 lakh crore rupees.

One year later that figure has come down by only ninety thousand crores meaning India’s PSU banks have bagged loans of over eight lakh crore rupees. Genuine business failure high profile escapes from India.

So much has happened in the last dozen years. It’s never black and white bad loan recovery under the insolvency and bankruptcy code is twice as much as the amount under previous mechanisms.

So something has improved. The problem has been recognized. But the fundamental problems remain. Several sectors are in debt. The economic cycle seems to be going through a downturn. The memories of wilful defaulters like Vijay Mallya are fresh.

There are allegations against bankers granting loans with vested interests. So where should the line be drawn? What about the scrutiny of such dodgy loans given without due process? Here again stringent law enforcement could be criticised.

The government may be accused of acting against bankers and auditors. Unnecessary use of force will only hurt the process but there can be no doubt that the law must take its own course.

The extent of bad loans and India’s banks is huge there are and will be questions asked of the bankers and some of the businesses and it’s the job of the government to keep the economy in check and to maintain the rule of law as recovery of bad loans improved. It’s a lesson that we must not forget indiscriminate lending and phony capitalism brought us here.