With unemployment on the rise and the economy in a nosedive, there seems to a general sense of anxiety especially among the youth with regards to their future prospects. We are almost past halfway through 2020 and if the first six months were any sign of what’s about to come, then we have to be prepared.

One’s early adulthood arguably does play a very big role for the rest of their lives. This is the time most of us start to earn and make choices that can make or break our future lives. Without further ado, lets get into some tips which will make you a millionaire if you play your cards just right.

Get Experience While Studying

Lets face it, staying out of school is a risk which most Indians are not willing to take and for good reasons. The realisation that just college is not enough to be financially well off in life sets in quite late usually. However, one should see things for what they truly are.

Realistically, with the pressure of graduate education it makes sense to figure out what works best. If you are a student in India you have to follow a three step cyclic process to excel at working while studying.

- Earn Marketable Certifications.

In the day and age of automation, one simply can’t expect to get away with low effort repetitive jobs. You have to prove your worth to your employer by having sufficient training in skills that are market relevant. These may include certifications and training in emerging field to the likes of Artificial Intelligence and Digital Marketing. Obviously, this hugely depends on your particular interests and availability. So, with the most significant hurdle out of the way lets look into the most annoying one. - Actually Getting a Job!

Despite the simple title, this will be the step which will test your patience. I personally in my first year of college, applied to 2000 jobs, got shortlisted by about 200, got an interview call from just 20, and got an offer letter from 2. Now that is the ground reality. But it is quite a simple process really. With services such as Internshala.com and LinkedIn Jobs, it has become far easier to search appropriate jobs. My suggestion will be to keep your cool even though nothing turns up. Do unpaid jobs to build your resume. If you are patient, eventually you will crack the case and get that dream job or internship. - Leveraging your Position for Course Correction.

Not to get too bamboozled by the overly technical jargon but it is an often overlooked yet vitally important process. One of the most important reason I stress so much on getting a job as early as possible is because it allows you to properly understand job roles and whether they are a perfect fit for you or not. Our goal is to be a millionaire and of paramount importance to achieve that is to have a job that you love and you are capable of excelling at. Say you are in either or both of these situations, one where you are not climbing the growth ladder in the company because you are unable to do the work effectively and second where you are not feeling the drive to do this particular work. Well, what do you actually have to lose. Back to step one.

Now this process will, for obvious reasons vary greatly from one individual to another. But one this is certain, without a robust plan you won’t be anywhere. It is a known fact that employers always prefer individuals with work experience. Best thing about this whole scenario is, you have nothing to lose.

Avoid Consumer Debt

This should come as a no brainer and yet if there is such a thing as ‘guilty-pleasure’ this would be it. Racking up debt on your credit card when you quite simply cannot afford something will guarantee you a place in hell. Financial issues consistently rank high in terms of endemic stress creator. Debt is a doubled edged sword which if you know how to wield properly will rewards you tremendously but without that knowledge and its application, it becomes a threat onto its host.

To mitigate a disease, one must be diagnosed with it in the first place. That’s the most common failure, people don’t know they are drowning in debt until it spirals out of control. Here’s how you can have a better financial health.

- Get A Budget!

It is another thing we choose to ignore. We do know that we must have a budget, how many of us actually go ahead and maintain one? Budgeting achieves two functions, primarily it helps you gauge how much you can actually spend and binds you to that and most importantly it helps you realise your plans for the future by practising financial discipline today. - Have A Low Debt-to-Credit Ratio.

Also known as credit utilisation rate, this ratio shows how much of the available credit you are using compared to the total amount you have available. It is an indicator of your financial health and your credit score heavily depends on it. To avoid getting into a high Debt-to-Credit ratio, the one practice that makes sense doing is to actively monitor your credit card transactions and being smart about it. - Avoid Cash Advances.

Cash advance is a service provided by cred card issuers allowing cardholders to withdraw eligible amount of cash on a line of credit through credit card. This might come across as an alluring option but on an average you will end up paying up to 24% interest rate. A cash advance is one of the early stages of credit card debt. So, it is vitally important to steer clear of these debts.

Apart from this, it is also really important to be paying at least the minimum amount per month on time if not the full amount. Moreover, keeping good credit card habits also build up your credit score. But why at all worry about it?

Build a Healthy Credit Score

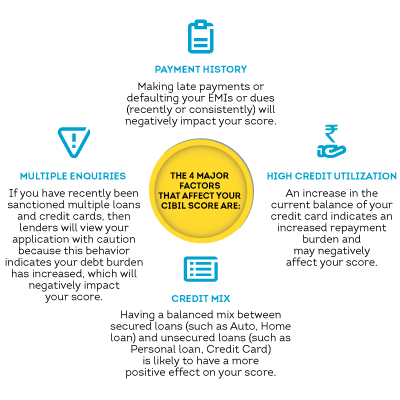

Considering you do all of the aforementioned practices just right and you have a very disciplined financial standing. But how can you grow your capital if you are not eligible for credit from banks and other financial institutions? For that reason it is important for you to have a healthy credit bureau score. In India TransUnion CIBIL Ltd. is the credit information company which maintains credit files on upwards of 600 million individuals and about 32 million businesses. Let us understand how CIBIL score works and why we even need it in the first place.

CIBIL score plays a determining role in the loan application procedure. It is sort of a first impression, an entry ticket to be eligible for credit based on how your practices in the past have been. A lower CIBIL score will sometimes result in immediate rejection of the application while a higher CIBIL score will give the lender more confidence in your application.

So, let’s understand how CIBIL score is calculated.

- It is a three digit numeric index of your credit history calculated from the ‘Accounts’ and ‘Enquiries’ section on your CIBIL report.

- The range is from 300 – 900 and higher is better.

So, how can you improve your credit score? Well, according to experts, here’s what you can do to improve your credit score.

- Avoid Late Payments

Often we avail credit facilities to help us with high ticket transactions like a car or housing purchase. While setting the terms of such loans it is vitally important for you to understand those properly and set EMI amounts which you can pay off on time. CIBIL takes late payments very seriously and it is the most important factor you should mitigate. - Eliminate Credit Card Balance

When you are the holder multiple credit lines, it becomes difficult to keep track of unpaid dues. However, it vitally important to do that and pay them off. To avoid situations like this, you must learn to spend on your credit card only as much as you can pay. Moreover, having more than three credit cards severely affects your ability to do so. - Do Not Close Old Debt Accounts

It may come as a non-intuitive idea after all that’s been said in the article. However, the minute you get your old debts paid off you should not be rushing to get old accounts removed from your credit report. Debt can be good if you have good practices. Good debt are ones which you have paid off in full on the repayment schedule. It is vital for your credit rating and one of the parameters CIBIL looks for is the history of said good debt. Thus, it will help you if you keep old debt and good account on the books to reflect a healthy repayment record.

Assuming that we have done these things correctly, we must find a mean to actually put ourselves in a position to have good financial health. Lets see what we can do to achieve this.

Live Below Your Means

I have previously dedicated an entire article to explaining the science and art of financial minimalism. In my experience, practising minimalism has had a profound impact not only on my finances but on my life in general. To better understand the reason behind the working of minimalism we have to delve a bit into psychology. The theory of Hedonic Treadmill otherwise known as hedonic adaptation is the positive tendency of humans to quickly return to a relatively stable level of happiness despite major positive or negative events and/or life changes.

In short, you are always bound to revert back to an average state of happiness no matter what happens in life. Overspending, much like binge eating or chain smoking is a very formidable foe. Adopting a minimalist lifestyle allows you to be ahead of such impulsive decisions and to

Here’s how minimalism can help you prosper financially while ensuring an unhinged standard of living in the cacophony of today’s society.

- Spend Only On Your Needs And Not Your Wants.

One of the core tenets of minimalism is to limit what you own. As mentioned in my previous article as well, owning only what you need will severely de-clutter your life and the same will be reflected in your finances as well. If you only spend on what you need and prioritise just on those things which are most important to you, it will have a net positive reflection on your finances as well. - Clear up Your Financial Clutter.

Among many things that minimalism is, it is first and foremost an art movement which has the sole focus of clean and clear aesthetics. Taking from the idea that less is more and applying it in all domains of life including your finances goes a long way in having a stress free situation. I have talked about budgeting before as well, consider budgeting to be financial mindfulness because it will help you see things which would have otherwise been invisible to you. that will help you see areas where you can cut down on your spending. All while keeping the most important expenses in mind while severing with the less important ones. - Simple Living, Simple Expenses

As we discussed previously, a minimalist lifestyle discourages over-consumption which happens to be the primary reason behind the debt crisis. Leading a minimalist lifestyle not only means you will be buying less, it also means you will be saving a lot on bills of repair, upkeep, maintenance, and electricity. That will instinctively result in a financially better off lifestyle.

With all that being said, it should be noted that minimalism in itself is a very difficult practice to get started with let alone master. Quite often I hear about individuals who have gotten frustrated and given up. To that extent, I would say that change of any kind is a difficult process. However we must change if we want to have different results than we current have. There’s an eye opener which can give you some drive and incentive to shift towards a minimalist lifestyle.

Track Your Spending

No matter how much we hate it, we have report cards in schools and colleges which serve the sole purpose of holding us accountable and grounded. When you start earning, there is no external agent to reflect your performance as an earner. That is why you need to have a budget and here’s how you can have one right now!

- Why Should You Have A Budget!

Now lets take into consideration the ground reality here. Starting a budget may seem all exciting but it is a very very difficult habit to incorporate. To not give up on your need to stick to the budget you will make, you have to assign reasons as to why you want it in the first place.

Some of the reasons why I have a budget are –

– I want to save more money;

– I want to reduce overspending;

– I want my spending to be in sync with my values and goals;

– I don’t want to spend money I don’t have;

– I want to stay out of debt; and

– I want to be on track with my long-term financial goals.You may have different reasons for adopting a budget but don’t forget that those who budget are almost twice as likely to report no financial worries and are very less likely to live paycheck to paycheck as a result of their strict grip on spending cycles. - Dissect Your Current Situation

Realism is a priceless virtue. You want to make a budget and not a wish-list. Experts over the world recommend a tracking period of at least 30 days to get a clearer picture of how much you do spend normally.

What I would recommend is that you take a month’s time before actually starting with budgeting. In this duration you will have to meticulously take note of every single expense you incur. To help you with this process apps such as Walnut, mTrakr, and Money View to name a few.

Since we are usually so caught up in everything that is going around that we seldom take note of our expenses. If you are to follow a budget, going through this process will go a long way in ensuring that you can actually be more financially conscious and ultimately have a higher chance of sticking with your budget. - Categorise Your Expenses.

From the previous exercise you would by now have a detailed list of your expenses. Now is the time to make the calculations. Bank of America and Khan Academy has put together a foolproof checklist which we shall take inspiration from.- Note your Net Income

It goes without saying that one of the most important step in making your budget will be to actually consider the amount of money you have coming in. This would come as a surprise but your net income is actually not the same as your salary. Your income includes dividends on your investments and taxes to name a few. While making a budget spreadsheet your final take-home income should be column one in terms of priority. - Define Your Goals

A rudderless boat is of no use to even the most seasoned sailor, in a similar capacity no matter how well thought out and minutely planned your budget is, it will serve no purpose if you don’t give it a direction to look ahead towards. You will have two types of goals: a) Long Term, & b) Short Term goals.

Your long term goals will pertain to things like retirement planning, family & children funds, etc. while your short term plans are not going to take more than a year to achieve. Say wanting to buy a vehicle or a vacation or reducing your credit card debt which I would highly recommend. Now once you have your income noted, goals defined, and expenses calculated, it is time to put all the ingredients of your budget together to make the pie. - Make The Plan

You already have a fair idea of how much you spend on a monthly basis and how much you earn. Based on your goals and plans you have to make adjustments which reflect your current spending habits while accommodating factors pertaining to your plans and income as well as risk tolerance.

To that extent it is generally considered to be fair to spend just about 60-70% of your monthly net income, lower the better. With that in mind, you will have to design your budget. - Micro-tuning

Now that you have a complete budget, you will take time to get adjusted to it. The various perks and nuances of being in that routine will be apparent to you only when you only when you start practising it. You will not achieve desirable results from day one. But whenever you think that you can maybe cut some costs here, or require more money to do something, you will have one of two options and choose whichever suits your purpose the best. You can either adjust your habits or your budget. Now from experience, changing your habits is almost always going to help you in the long run simply because your budget reflects what you want to be and changing that is akin to compromising with your plans and goals.

- Note your Net Income

Yes, this is all it takes to be up and running with a proper budget. And all of these will help you even out the odds in your favour. What will make you rich is your investments. Lets see how you can invest today to have a golden future tomorrow.

Invest!

Investments can sound very scary, but it an absolutely essential and simple concept which can be understood and practised by anyone. To be more clear about the topic, investing is all about taking the money you have and giving it to corporations and businesses who can utilise that money to expand their operations and in return give you the returns of heightened profits.

In the modern era, the opportunities are endless and here’s how you can become a millionaire only by your passive incomes-

- Start Early because, Compound Interests.

A common mistake lot of us make is to assume that we have a lot of time on our hands when we are in our 20’s. That might be true when it comes to lifelong liabilities such as marriage and kids, but certainly not when it comes to building your assets. With our goal to becoming a millionaire in mind, lets assume that you start investing $ 300 per month when you are 20 and do not stop till you are 60. Taking a very conservative figure of 8% return during that time, you will own more than $ 1 Million by your 60’s. This is not considering that as your progress with your career you will invariably end up earning and investing more. However, lets say that you start this very same process at the age of 30, by the time you were 60, you will end up with $ 440,445 only! Staving off investing for 10 years will save you $36,000 initially, but that amounts to more than half a million dollars in net losses.

The reason this is the first point is because all the other markers in this list can be altered, but time once wasted cannot be bought back anyhow. So, keep this in mind and start today! - Know your options.

This is the most exhaustive process when it comes to investments. However with information readily available for just about anything and everything, it is not nearly as difficult as it once was to get started. So, let’s dive in to explore our options.- Tax Free Investments

It is tax season and nothing hurts more than giving away your hard earned income to government agencies. So, here’s give options for you to skimp on taxes while being on the road to becoming a millionaire-

Firstly we have Life Insurance which we all know about. Now one thing that most of don’t understand that life insurance doesn’t cover upon death, it covers for major life goals such as marriage and buying a house or your child’s education as well. Maximum annual investment of ₹ 1.5 Lakhs can be considered as tax write-off. Then we have other investment schemes such as PPF (Public Provident Fund) and NPS (New Pension Scheme) which are both government sponsored savings and retirement planning direct tax free investments. PPF returns are linked to the debt market and has a lock in period of 15 years while NPS gas the same quirks with the difference being that your money under NPS is managed in three separate accounts with distinct asset profiles i.e. Equity (E), Corporate Bonds (C), and Government Securities (G) and investors have the choice of actively or passively managing their portfolio. It has the same investment cap of 1.5 Lakhs.

These are reasonably risk free investments and are thus not very high on returns. In your early years it is wise to have an investment strategy a bit more on the aggressive side. So, lets explore those options. - Index Funds

If you’ve read my answers before, you will know that I am an avid enthusiast of index funds. The reason why index funds are such a favourite among investors of all classes are because of the diversification and safety net it provides. An index fund imitates the stock market (NSE, Nifty, Sensex, DJI Average, etc) in a passively managed portfolio which hugely decreases the risk of your investment going sour.

Lets understand with the help of an example.

Suppose you have $ 100 which you want to invest. You have two options, you can either buy one property which hypothetically costs $100 or you can choose to buy 1% of 100 houses. Let’s say you go for option one and bout one house for $100, the fundamental problem with this investment is what if due to some issue like an earthquake or flood, that house turns into a bad investment and you loss $100. But, in the second scenario, even if due to any reason you lose one house which you had a 1% stake in, you still have 99% of your investment to keep giving you dividends. That is why index funds are such a great and carefree way to invest.

Experts around the world recommend an investment horizon of at least 7 years for index funds and a conservative average in terms of returns is at least 10-12%. There is a perk to investing long term other than compounding interest working its magic and that is tax benefits on Long Term Capital Gains which is tax exempt up to One Lakh Rupees.

Moreover, investing in index funds is the easiest to do simply because of the fact that it is passively managed and requires no research. - Dividend Paying Stocks

Any for profit company has multiple channels to use its profits, one of the two things that a company does with its profits is to either use that money for enhancing it’s operations and expanding and/or distributing the profits among its owners and shareholders.

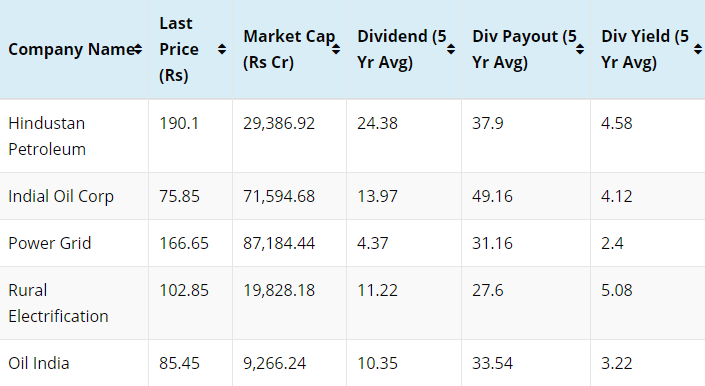

A dividend is a distribution of a portion of a company’s earnings, and mostly big and well established companies give decent dividends to their shareholders. Usually this payout happens twice a year namely during the interim dividend and final dividend. These stocks are the favourites of investors like Warren Buffet who prefers value investing over anything else.

Dividend paying stocks are the best pick for investments especially after the pandemic because a regular dividend is the sign of a healthy company and more importantly it is almost always the large cap companies which are in a position to pay out dividends.

Here’s top five dividend paying stocks in India-

- Tax Free Investments

The Bottom Line

With all that being said, turning over your lifestyle completely is not an easy process. It requires intense discipline and extraordinary willpower to go through the whole process. But, it is possible and if you can treat money like a slave instead of having it be your master, you can rise above the rest and secure a place in the coveted 1% position.