Despite being just a third-world developing country paving its way all along, dealing with difficult neighborhood, burgeoning population and tricky geopolitics, India has managed to snatch away some limelight always.

Be it the Non-aligned movement, wreathing diplomacies in Korean war, its role as a staunch antagonist to terrorism, a rehabilitator in Afghan crisis or a commander in war against Climate change, India made sure that its position in World order is recorded right.

International Solar Alliance (ISA) has further consolidated India’s stand for climate action.

Under Paris agreement 2015, India made a voluntary commitment to install 175 gigawatts (GW) of renewable capacity by 2022. In 2021, the current installed capacity is only 95 GW, a little more than half the target.

With just a year left and Covid grabbing all the attention, India may rather miss its immediate target.

It’s not just this case that’s troubling but the uncertainties in Indian policies governing Solar power dynamics.

Fickle contracts shadowing the solar power sector:

It has already been estimated that with increasing ease of generation, the cost of solar power may fall significantly to of Rs 1.90 per kWh by 2030 making India one of the cheapest producers of solar electricity. Every year, it has been recording a 18 percent decline in solar tariffs.

But everything seems uncertain with the renegotiation of pre-determined contracts including the Power Purchase Agreements (PPAs) between State governments and power producers.

These PPAs are otherwise, composed after a proper bidding procedure. Many state governments are now exploiting these terms in order to achieve a lower price per unit of electricity since last two years.

It is a potential threat to the sector as experts believe that this may derail India’s long-term journey towards attainment of green energy by eroding the confidence of investors.

Taking examples to Understand the scenario:

As per the targets set by Union Ministry of New and Renewable Energy for Uttar Pradesh, the state has an installed capacity of 3,878 megawatts (MW) of renewable energy against supposed target of 14,221 MW by 2022, including 10,697 MW of solar power.

However, recently UP cancelled the solar auction for instalment of 500 MW solar power. The auction quoted an early price of Rs. 3.17-Rs. 3.18 per unit but in another auction, a price of Rs. 1.99 per unit was finally realized.

This may help the state fetch a lower price for the same amount of electricity produced but these shallow changes are only delaying the bigger target while blatantly neglecting the growing Industry’s needs.

Even other states such as Andhra Pradesh, Rajasthan, and Gujarat have taken the same recourse.

It is to note that cancellation can happen in any of the known four phases – before RA (reverse auction), after RA and before LOI (Letter of Interest) issued, between issuance of LOI and the PPA (Power Purchase agreements) and after the PPA.

Uncertainty looming, Investors get insecure:

Director Energy finance studies at Institute of Energy Economics and Financial Analysis (IEEFA), explains: “if the states are cancelling the PPAs purely because the prices of solar dropped, then that is an abuse of the legal position. It really undermines the whole balance of power”.

“When you’re actually doing tenders … you’ve got to treat investors fairly and equitably. And if (they play) heads you win, tails they lose, investors aren’t going to play that game.”

An Energy economist explains: “The per-unit price for solar power has gone down and they are expected to further decline with better technology and finance options in future. But that does not mean that states can keep cancelling the PPAs – especially when they are on an actual cost basis at that point of time”.

A part of its credit can go to the reverse auction scheme that has been constantly in use for solar PPAs. In Reverse auctioning, suppliers compete for the buyer’s business proposal by underbidding one another under extreme competition.

As different suppliers compete to win the tender and lowest prices are taken over, it tends to be risky and controversial for intimidating suppliers.

Although reverse auctioning is not considered a problem globally, its implementation failures are pushing the sector deep down, as this creates confusion and uncertainty among the power developers if their plan to generate power and materialize their investment back will be accomplished or not.

An NPO official provides an example: “at the end of the previous fiscal year (2020-21), nearly 26 GW of projects were under various stages of bidding” and “project developers are second-guessing if their bids will actually see the light of the day.”

“This is surprising and ironic because the developer and investor community had raised concerns about future investments in the state. Instances like these may encourage off-takers to keep the option of renegotiation/cancellation open in the future.”

Has the Government been apprised of this threat to its aspirations?

Yes, the government knows it all but not concerned enough until there is tangible impact.

Despite the disturbing trend observed, the issue has been brought to light by a parliamentary panel observing that “long term Power Purchase Agreement (PPA) has become a conundrum.”

The panel said: “Since the advent of solar power, its tariff is on a constant decline. In recent years, solar power tariff has aggressively been quoted making the Discoms (power distribution companies) reluctant to enter any long term PPA.”

“This situation is causing disruption as long-term PPA is a pre-requisite for financing any new power project. In absence of long term PPAs it may be difficult to attract investment in the power sector.”

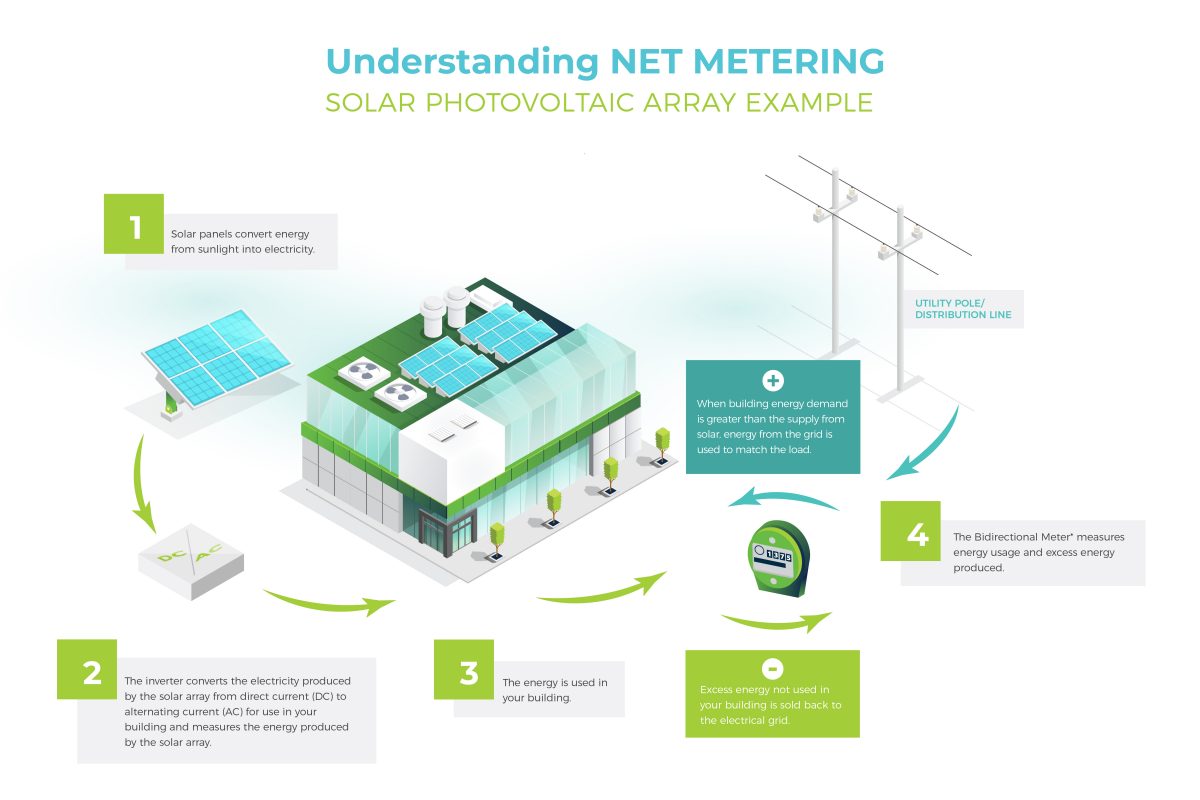

Grid integration and net-metering procedure used in India becomes even more difficult with poor financial condition of Distribution Companies (DISCOMs).

A chain reaction: policy loophole, doubtful Investors and fading FDI

Even during covid times, international investors’ appetite for made-in-India renewable energy has been more resilient than any other sector.

FDI coming in the renewables sector were down just 24% year on year, even outperforming the UNCTAD’s prediction for that year.

It is important to note here that in order to achieve 450 gigawatts (GW) of installed renewable energy capacity by 2030, the country will require fresh investment of $500 billion.

On the similar lines, International Energy Agency’s (IEA) Energy Outlook 2021 has estimated $1.4 trillion required for funding the low emission technologies for attaining sustainability in next 20 years.

Unable to deal with uncertainty and certain underlying Indian problems like land acquisition and grid access problems, SoftBank, a Japanese multinational conglomerate and also a major investor in India’s renewable sector, pulled out in may 2021.

A bigger problem is ready to encounter us on that very path if these small but serious concerns are not addressed and eliminated as India’s energy demand is slowing down for the past two years engulfed in the lockdowns and pandemic hits.

Timely implementation and rigidity to the well-established norms of contract can help, for starters.

“At the end of the day, the casualty is the industry and we may lose investors, projects and even valuable time while we are running against the targets. All we ask from the industry is clarity and withhold the sanctity of contracts”, urges an expert from NSEFI (National Solar Energy Federation of India).

Apart from domestic perils in solar power-driven sustainability, there are challenges India is facing on International for a like WTO where US challenged India’s solar policies. Although India has won the case but several issues remain.

Every good work is bedeviled with challenges of its own, it’s important that these are nipped in the bud and does not become a stigmata.