Pradhan Mantri Mudra Yojana is a scheme initiated by the Narendra Modi government on 8th April 2015 to provide loans up to Rs. 10 lakh to non-corporate, non-farm small/micro-enterprises. The main aim is to “fund the unfunded” and enable a small borrower to borrow from all the Public Sector Banks.

MUDRA stands for Micro Units Development and Refinance Agency.

Under the Mudra loan scheme, people involved in non-farm activities can avail loan up to Rs. 10 lakh. Private Sector Banks, Non-Banking Financial Companies (NBFCs), Micro Finance Institutions (MFIs), Public Sector Banks, Regional Rural Banks (RRBs), State and Urban Co-operative Banks and Foreign Banks are eligible to provide loans under the scheme.

The official website for Mudra yojana- Mudra.org.in

Contents

Background

It was realized that the small businesses were unable to develop to their full potential as the country’s banking system was unable to meet their peculiar demands of small businessmen. Furthermore, the scattered approach to small business models was causing a rise in logistics cost.

Therefore, the government of India came out with PM Mudra yojana to cover such entities to the formal banking system and help them avail of loan benefits.

Objectives

- To refinance collateral-free loans provided by the lenders to small borrowers.

- To bring small enterprises such as NCSBS (Non-Corporate Small Business Sector) and ‘own account enterprises’ under the folds of the formal financial system

- To extend the affordable credit to MSMEs.

- To provide integrated financial support to the micro-enterprises sector.

- To integrate the informal economy into the formal sector.

- To monitor the micro-finance institutions.

- To generate employment avenues in these micro-units.

Loan offers

The scheme has three categories under which loans are disbursed:

- Shishu – For loan amount up to Rs. 50,000

- Kishor –For loan amount from Rs. 50,001 to R.s 5 lakh

- Tarun – For loan amount more than 5 lakhs and up to Rs 10 lakh

The loan schemes have been named ‘Shishu‘, ‘Kishor‘ and ‘Tarun‘ to emphasize the level of growth and funding needs of the beneficiary unit.

Under the guidelines of the MUDRA scheme, it would be ensured that at least 60% of the credit flows to ‘Shishu’ Category Units. There will be no subsidy for the loan given under PMMY.

Sectors covered

- Land Transport Sector / Activity – Purchase of transport vehicles for goods and personal transport such as auto rickshaw, small goods transport vehicle, 3 wheelers, e-rickshaw, passenger cars, taxis, etc.

- Community, Social & Personal Service Activities – Such as saloons, beauty parlors, gymnasium, boutiques, tailoring shops, dry cleaning, cycle, and motorcycle repair shop, DTP and Photocopying Facilities, Medicine Shops, Courier Agents, etc.

- Food Products Sector – Papad making, achaar making, jam / jelly making, agricultural produce preservation at rural level, sweet shops, small service food stalls and day to day catering / canteen services, cold chain vehicles, cold storages, ice-making units, ice cream making units, biscuit, bread and bun making, etc.

- Textile Products Sector – Handloom, power loom, chikan work, zari and zardozi work, traditional embroidery and handwork, traditional dyeing and printing, apparel design, knitting, cotton ginning, computerized embroidery, stitching and other textile non-garment products such as bags, vehicle accessories, furnishing accessories, etc.

Eligible beneficiaries

Any businessperson or business who/which has not been a defaulter on any loan repayment previously is eligible to borrow under the Pradhan Mantri MUDRA Yojana. Any such individual business owner, private limited companies, public sector companies, proprietary firms or any other legal business entity can apply for the Mudra loan.

Purpose of Loan assistance under PMMY

The loan amount cannot be used for personal needs. The sum of the money can only be used for specific activities in the manufacturing, services or trading sectors. Businesses can also utilize the capital obtained from a MUDRA loan for marketing purposes. The maximum repayment period for a MUDRA loan can extend to 5 years. But the repayment period can be shorter if the lender decides so when sanctioning the loan.

For availing loans under the PMYY scheme, there will be no processing fee or requirement of collateral.

How to apply for PM Mudra Yojana

Borrowers have to approach the local branch of any of the financial institutions in their region. They have to verify their documents and as per the eligibility norms of the respective lending institutions, the loan amount as assistance will be sanctioned to the beneficiaries.

Documents to be submitted along with the application

- Proof of identity– Self-attested copy of Voter’s ID Card / Driving Licence / PAN Card / Aaadhaar Card / Passport / Photo Ids issued by Govt. authority etc.

- Proof of Residence- Recent telephone bill / electricity bill / property tax receipt (not older than 2 months) / Voter’s ID Card / Aaadhar Card / Passport of Individual / Proprietor / Partners Bank passbook or latest account statement duly attested by Bank Officials / Domicile Certificate / Certificate issued by Govt. Authority / Local Panchayat / Municipality etc.

- Applicant’s recent Photographs (2 copies) not older than 6 months.

- Quotation of Machinery / other items to be purchased.

- Name of Supplier/details of machinery/price of machinery and/or items to be purchased.

- Proof of Identity / Address of the Business Enterprise – Copies of relevant Licences / Registration Certificates / Other Documents pertaining to the ownership, identity of the address of the business unit, if any

- Proof of category like SC / ST / OBC / Minority etc.

Offers under Pradhan Mantri MUDRA Yojana

- Micro Credit Scheme – Under this scheme, financial support is extended through Micro Financial Institutions (MFIs) so that they can provide business loans of up to Rs. 1 lakh.

- Women Enterprise Programme (Mahila Uddyami Yojana) – It is specifically at women entrepreneurs. The scheme is envisaged to encourage individual women entrepreneurs, women’s Joint Liability Groups and Self-Help Groups.

- Refinance Scheme for Banks – MUDRA scheme also allows banks to easily refinance loan amounts. Such banks include Scheduled Co-operative Banks, Regional Rural Banks, and Commercial banks. The refinance facility is available only if these business loans have been extended for microenterprise activities.

- Mudra Card – It is an innovative tool under which makes credit is made easily accessible to small businesses. It can be used as a credit card with an overdraft (loan) limit. The card can also be used as a debit card with the facility of ATM withdrawals.

- Credit Guarantee Fund – It is also known as the portfolio credit guarantee that allows eligible entities to receive micro-loans with ease. It involves the creation and use of a special fund termed as the Credit Guarantee Fund for Micro Units. This fund is managed by the National Credit Guarantee Trustee Company Ltd. and

- Equipment Finance Scheme – It enables small entrepreneurs and micro-units to avail of a loan to finance the purchase/upgrade of qualifying equipment/machinery. This encourages enterprises to improve their production techniques to increase the overall productivity and efficiency of their business.

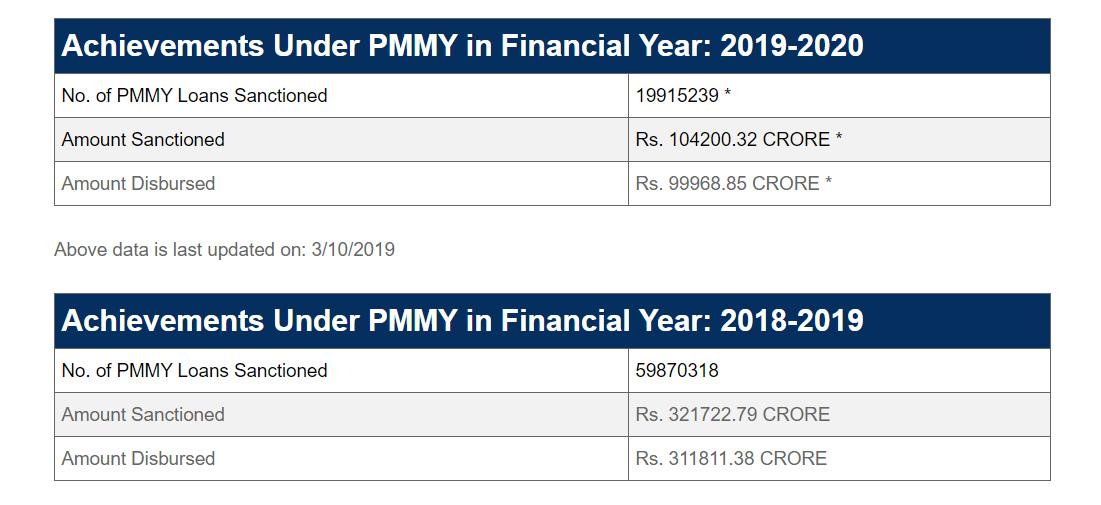

Progress Card of MUDRA Scheme

Conclusion

With the inception of Mudra Yojana, the government has finally integrated the small micro-units into the formal credit system. The unbanked population that was earlier handicapped by the shortage of funds, is now able to meet their livelihood demands.

Such micro and small units are where the true India resides. Therefore, the development of these units is the real index of economic transformation, and this process is being achieved by Mudra Yojana very well.

SAR NAKU LOAN EPPINCHANDI