Health emergencies aren’t notified beforehand. With sedentary lifestyles, increasing numbers of people in India become prone to lifestyle diseases.

And the medical treatment has now become quite expensive, especially in private hospitals, due to the increased demand for quality healthcare services. And the hospital bills are enough to drain one’s savings, without insurance.

Therefore, a comprehensive care program is an essential requirement because it provides compensation against the exorbitant hospitalization costs in the case of an injury or sickness to the covered family members and the policyholder.

In addition to the medical coverage, health insurance plans also offer premium tax benefits under section 80D of the Income Tax Act, 1961.

When it comes to choosing the best health insurance scheme for us or our family, we’re all clueless most of the time. When we consider buying one, we generally can’t fix particular health insurance. To get the weight off your back, I’ll send you a peek at the 10 five health care policies you’ll need to start having.

Contents

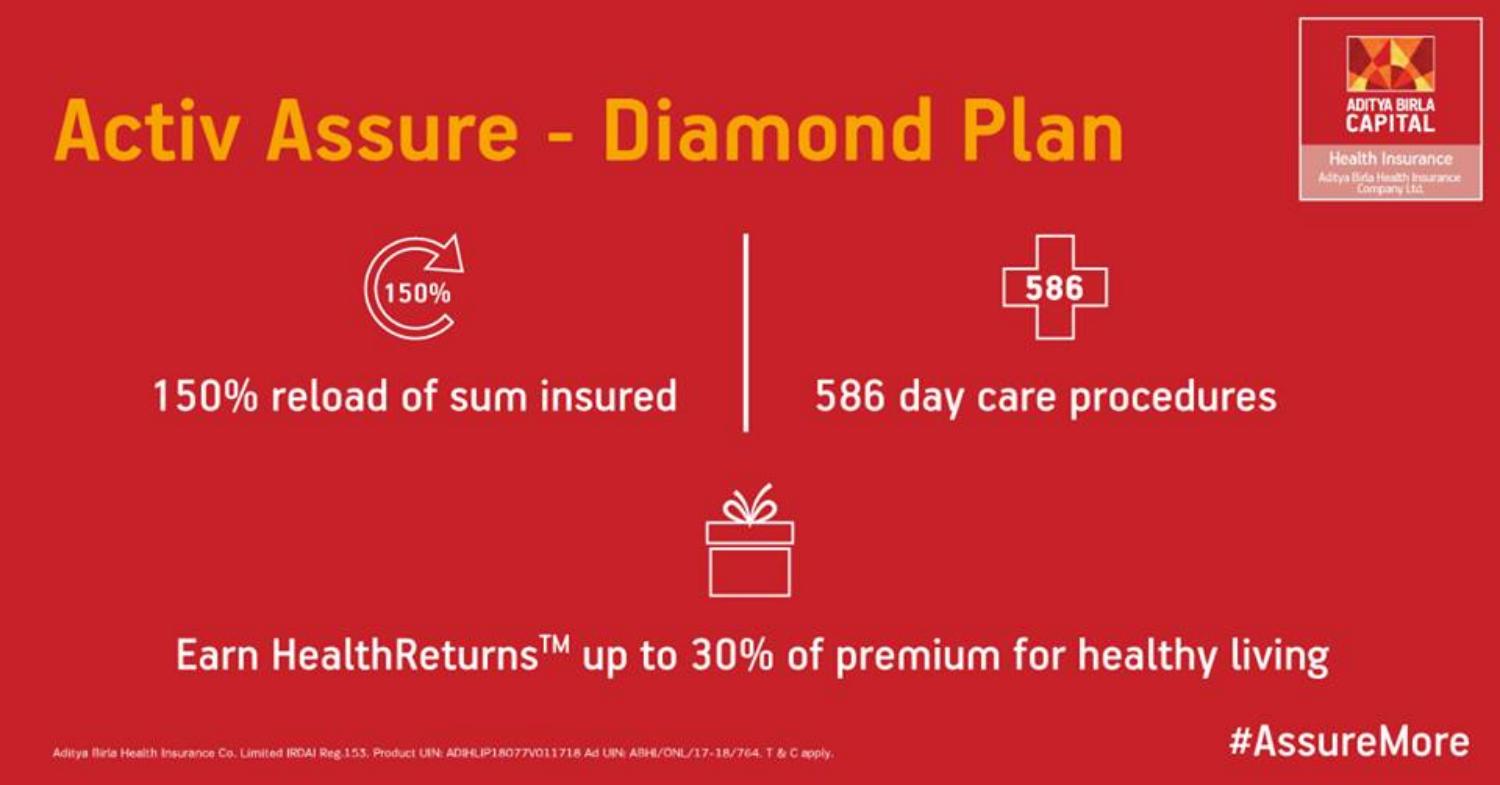

1 Aditya Birla Activ Assure Diamond Plan

The Aditya Birla Activ Assure Diamond program is a premium health care package launched by Aditya Birla Capital for persons pursuing affordable benefits at a higher deductible number. This includes professional hospitalization costs as well as second advice on serious condition and disaster response programs at home / international stage.

The health care package also includes an extra cancer hospitalization support plan, every space expansion, and a decrease in the screening time for pre-existing diseases.

Plan Inclusions and Exclusions

1.1 What’s Included

- Products with overseas / domestic medical services such as air ambulance etc.

- To keep active and safe, receive HealthReturns worth up for 30 percent of your price.

- Offers 150 percent reload of the insured sum for subsequent claims due to unrelated illness, maximum up to Rs. 50 Lakh.

- Provide coverage over 24 hours for in-patient hospitalization due to a planned treatment or an emergency.

- Coverage with 586-day nursing treatments even though there are fewer than 24 hours of hospitalization.

1.2 What’s Not Included

- Illness or disability accordingly is caused by any venereal or sexually transmitted disease.

- Injury or disease-induced especially by any product, intoxicant, medication, marijuana, or hallucinogen.

- Every pre-existing illness or disability that results from a pre-existing condition, or some accident that occurs from it.

- Death, injury, or disability resulting from an act of enemies from abroad, war operations, civil war, etc.

- Attempted suicide, accidental self-inflicted harm, self-destructive behavior, etc.

1.3 Features and Benefits of Active Assure Diamond Plan

|

Features/Plan |

Activ Assure Diamond (2, 3 Lakh) |

Activ Assure Diamond (5 to 200 Lakh) |

|

Restoration Benefit |

150% of SI | 150% of SI |

|

No Claim Bonus |

Up to 50% of SI | Up to 50% of SI |

|

Room Rent |

Up to 1% of SI |

Single private AC room |

| ICU Charges | Up to 2% of SI |

Actual |

|

Pre and Post Hospitalization |

30 & 60 days | 30 & 60 days |

| Day Care Procedure | 586 |

586 |

|

Free Health Checkup |

Available |

Available |

|

Organ Donor |

Up to SI | Up to SI |

|

AYUSH |

Up to Rs. 15000 |

Rs 20,000 for SI 5-10 Lakh; Rs. 30,000 for SI 15-40 Lakh; Rs. 40,000 for SI 50-75 Lakh; Rs. 50,000 for SI 1-2 Crore |

| Domiciliary Hospitalization | Up to Rs. 50000 |

Up to Rs. 50000 |

|

Ambulance Cover |

Up to Rs. 1500 per hospitalization |

Rs. 2000 for SI 5-10 Lakh; Rs. 2500 for SI 15-40 Lakh; Rs. 3000 for SI 50-75 Lakh; Rs. 5000 for SI 1-2 Crore |

|

Second Opinion |

Available for 15 critical illnesses |

Available for 15 critical illnesses |

2 Bajaj Allianz – Health Infinity

Bajaj Allianz Health Infinity Plan is a comprehensive health insurance plan that offers a wide range of benefits in the case of hospitalization due to illness or injury to take care of the medical expenses associated with you and your family.

The Bajaj Allianz Health Infinity Policy takes into account the additional costs incurred by an individual during hospitalization, thereby falling many times short to cover many expenses under a normal insured sum. Bajaj Allianz acknowledges this problem and the organization has come up with a new Health Infinity Policy strategy to tackle this question.

2.1 Main features of Health Infinity Policy

- Guaranteed Plan – No Health Insurance Plan or Insured Sum.

- Individual plan – Self, partner, children, and parents individual plan.

- New concept- A new idea to select the health plan according to the daily room rent and coverage will be 100 times – details given in the next section.

- Cost Sharing – When the permissible sum reaches 100 times the room rent option, the 15%/20% and 25% co-payment, as chosen, would be added to the claim sum information provided in the next section along with room rental choices.

- No Sublimit – There is no sublime for in-patient hospitalization.

- Pre-hospitalization-A 60-day benefit for pre-hospitalization expenses.

- Post-hospitalization – 90 days benefit to cover post-hospitalization expenses.

- Ambulance-Roadside service for INR 5000 for every hospitalization.

- Child care process – Providing sufficient child care.

- Medical check-up – Precautionary health check-up every 3 policy years, equal to room rent/day as picked, but maximum up to INR 5000, whichever is lower.

- No Health Test – Medical pre-policy research is not needed until 45 years.

- Pre-existing illness-Pre-existing disease risk within 3 years in the 1st Medical Program.

- In-house dispute arbitration – The organization has a mediation department and no participation of third party TPA.

- Health Gain-Income tax Profit for utilization in an insurance benefit under section 80D.

2.2 Eligibility

|

Entry age |

18 years to 65 years Children: 3 years to 25 years |

|

Road Ambulance |

Up to Rs. 5000 |

|

Policy tenure |

1 year, 2 year or 3 years |

|

Waiting period |

36 months |

2.3 Discounts under Health Infinity Policy

- Discount for Wellness: A 5 percent discount on a renewal is given upon submission of certain specified documents.

- Long-term plan discount: 4 percent discount for policy 2 years and 8 percent discount for policy 3 years.

- Family plan discount: if 2 or more entitled family members are covered, a 5 percent discount will be given.

- Bajaj Allianz General Insurance: If the plan is purchased online, a 5 percent discount will be given.

- Employee discount: The employees working in Bajaj Allianz receive a 20 percent discount.

2.4 How to file a claim for Bajaj Allianz Health Infinity Policy

2.4.1 Cashless Claim

With the cashless allegation, the policyholder’s care must be performed only via either of the network hospitals that come under the Bajaj Allianz General Insurance Company. The steps below.

- Inform the insurance company or TPA on the desk at the hospital.

- First, you have to complete the pre-authorization form that is available at the insurance desk at the hospital. Display your insurance card for Bajaj Allianz Health Insurance too.

- The form should be sent to the Company by email or fax.

- A letter of approval will be sent from the Bajaj Allianz General Insurance claims management (that means your claim is accepted).

- Now the company or TPA will handle the hospital bills directly.

2.4.2 Reimbursement Claim

- Download the claim form from the company’s official website, or take it from the company’s nearby branch.

- Give the application to the client or TPA along with the appropriate documentation such as discharge report, medication, etc.

- When the claim form is issued by the organization, the same would be analyzed by the staff.

- The firm will transfer the funds directly to your bank account in the case of an approved claim.

Religare Care NCB Super is a comprehensive health insurance plan which has an exceptional increase in the Sum Assured No Claim Bonus. Other unique features of coverage include Sum Assured auto restoration, Alternative treatments (AYUSH) benefit, free health check-up, daily cash allowance, ambulance cover, home treatment cover, etc.

3.1 Benefits included

Hospitalization means any impatient treatment (min. 24 hrs stay) as well as the 541-day treatment procedures mentioned

- Hospitalizations related to accidents are covered from day 1.

- Other hospitalizations after 30 days are covered. Cover begins after 30 days, except in case of accidents covered from day 1

- Exceptions: any pre-existing diseases (PED) covered after 4 years, and certain specified diseases covered after 2 years from the start date of the policy.

3.1.1 Other additional benefits:

- Restauration 100% Cover.

- No Bonus Claim.

- Free check-up on health.

- Charges relating to the ambulance.

- 30 Days before hospitalization.

- 60 Days after being hospitalized.

- Costs on donor organs.

- Home Therapy.

- Therapy with Ayush.

3.2 Out of pocket expenses

- You will bear all those expenses that are not covered by the policy. Please refer to the list of such expenses in the Exclusions section below

- Additionally, if you are staying in a space tier above Single private room, you would have to pay extra.

3.3 Claims settlement

- If you go to a non-network hospital, by providing the insurer with the original bills and documents, you will have to get the claim settled on a refund basis.

- When you are referred to a network facility, you will obtain the insurer’s cashless consent and the insurance can then cover the bills jointly with the doctor. See the chart below for the network hospitals near you.

4 Digit – Option 3 Super Care

GoDigit General Insurance Company’s Digit Health Plus Policy protects you and your family by delivering extensive coverage of the plan. The policy comes with a wide array of benefits and features to meet everyone’s healthcare needs and expectations. The holistic strategy allows policyholders to compensate people or households with pre- and post-hospitalization costs.

It also provides coverage for maternity expenses, treatment for critical illness, outpatient dental treatment, and much more. You will protect yourself, your family, dependent children, and so many others with this policy in mind. Within this policy, people between the age group of 1 year and 60 years may be covered.

Plan Inclusions and Exclusions

4.1 What’s Included

- In-patient treatment covers such as room rent, ICU, physician fee, etc.

- Expenditures sustained at pre- and post-hospitalization.

- Hospitalization as a result of maternity treatment and other associated costs.

- Natural medicine (AYUSH), organ donation, medication for infertility.

- Treatment of outpatients (OPD), i.e. without hospitalization costs.

- Treatment of critical illness or undergoing surgical procedures covered.

4.2 What’s Not Included

- Hospitalization is attributable to a disorder that does not suit the medication issued by the doctor.

- Maintenance of artificial life including the use of life support machines.

- Medical expenses arising from participation in any unlawful or illegal or criminal act.

- Pre-existing illnesses until the period of waiting is over.

- Suicide or suicide attempts due to insanity, narcotics, drugs, or alcohol abuse.

- Prenatal and postnatal medical expenses, unless hospitalization results.

|

Situations |

Restoration under Complete Use of Sum Assured (INR) |

Restoration under Part Use of Sum Assured (INR) |

|

Sum Assured |

4 lakhs | 4 lakhs |

| Claim Number 1 | 3.5 lakhs |

3.5 lakhs |

|

Remaining Sum Assured |

50,000 | 50,000 |

| Claim Number 2 | 70,000 |

70,000 |

|

Restoration Benefit |

No | Yes – 4 lakhs |

| Claim Number 2 Paid | 50,000 |

70,000 |

|

Total Claims made in a year |

420000 | 420000 |

| Total claims paid with a health plan in a policy year | 4 lakhs |

4,70,000 |

5 Future Generali – Health Total Vital

Future Generali Health Total is a comprehensive health plan for retailers with wider and longer coverage. The scheme comes with lifelong renewability and is accessible on a client and family floater basis. Health Total plan provides pre-hospitalization coverage, post-hospitalization, maternity expenses, baby-related procedures for newborns, and others.

The Health Total plan comes in three variants with different sum assured levels, namely Vital, Superior, and Premium.

Plan Inclusions and Exclusions

5.1 What’s Included

- E-Opinion regarding illness or injury and alternative therapy.

- The scheme includes costs borne by organ donors.

- Maternity costs are also covered.

- Coverage of treatment costs paid at non- and post-hospitalization.

- Coverage for the daycare treatment and organ donor expenses.

5.2 What’s Not Included

- Drug abuse, self-inflicted injuries, HIV / AIDS & STDs

- A cosmetic and plastic treatment

- Congenital pathological abnormality and associated illness/defect

- Any admission to hospital for investigative/diagnostic purposes

- An injury-induced directly or indirectly by the battle, attack, an act by a foreign adversary, and so on.

5.3 Critical features of Future Generali Health Total Vital Insurance Plan

5.3.1 Room rent

- Limits put on leasing costs for the bed and ICU.

- Such proposals include no Space Cap Number.

5.3.2 Co-Pay

A specific percentage of the amount of the allowable claim to be borne by the Insured.

If an insured joins the scheme at the age stated in the chart, the corresponding co-payments would occur to every valid allegation.

— 60yrs to 64yrs: co-payment of 20%.

— 65yrs to 69yrs: co-payment of 25%.

— 70yrs to 74yrs: Co-payment of 30%.

— 75yrs & above: Co-payment of 40%.

5.3.3 No Claim Bonus

- Health insurance plans may provide Cumulative Premium in which, at the point of redemption, the Amount Insured is raised by a certain amount on each additional year of coverage.

- 50% of the minimum amount insured up to a limit of 100% for any year of non-payment (the accumulated benefit is decreased by 50% of the sum insured after the claim is made).

5.3.4 Pre-Existing Diseases

This means any condition for which you had signs or symptoms and/or were diagnosed and/or received medical advice/treatment within 48 months of the insurer’s first policy.

This plan has a waiting period of 4 years for 100 percent of the admissible claim amount in the case of pre-existing diseases.

In the case with pre-existing conditions, this program often includes a processing time of 2 years but only payable 50 percent of the value of the petition.

5.4 Eligibility Criteria

- Required Entry Age:- Year 1.

- Average Entry Age:- Kids-91 to 25 years / Adults-18 years.

- Renewal Age:- Renewal for a Career.

- Sum Insured:-Vital Plan-3 Lakhs, Lakhs 5, Lakhs 10.

- Tenure policy:- 1 , 2 & 3 years.

- Description of family:- Vital Plan-Self + Spouse + 2 Children + 2 Parents (1 + 5).

- Premium Calculated based on:- Age (i.e. number Selected as Insured).

5.5 Working of the Future Generali Health Total Plan

- The policyholder chooses the option for the plan and the Sum Assured and decides if he wants an individual plan or a floater.

- There are three types of the plan with different levels of Sum Assured and covered by various members which are as follows:

|

Plan Types |

Sum Assured range |

Members covered under the floater variant |

|

Vital |

Rs.3,5 and 10 lakhs | Self, spouse, dependent children aged up to 25, and dependent parents. |

| Superior | Rs.15,20 and 25 lakhs |

Self, family, dependent children up to age 25, dependent or non-dependent parents, dependent spouses, daughter or son-in-law, mother-in-law, grandparents, and grandkids. |

|

Premier |

Rs.50 lakhs and Rs.1 crore |

Self, spouse, dependent children up to age 25, dependent or non-dependent parents, dependent siblings, daughter or son-in-law, parents-in-law, grandparents, and grandkids. |

6 HDFC ERGO – My health Suraksha Smart Plan

My: HDFC Ergo’s Health Suraksha Plan is a choice you can’t ignore when it comes to health insurance policies. It is a plan that offers multiple insured sum options ranging from Rs. 3 Lakh to Rs. 75 Lakhs and is available as Silver Smart, Gold Smart & Platinum Smart Plans under three variants.

As the name implies, this package is built to include every age entry opportunity and lifelong renewability cover for individuals. The package is offered at affordable rates and robust coverage and the option of charging an average fee in equivalent installments of 3, 6, and 12. Under this plan is also offered the long-term policy option up to 3 years with an attractive premium rate.

6.1 Types Of my: health Suraksha Smart Plans

Under my scheme, HDFC has three variants: wellness Suraksha Smart Plan.

- A Smart Silver Program

- Smart Gold Program

- Platinum Smart Project

Individuals who follow the qualifying requirements set out in the table will buy a package of their choosing.

Plan Inclusions and Exclusions:

6.2 What’s Included

- Hospitalization in the hospital includes.

- The cost of pre- and post-hospitalization.

- Blood donation compensation costs.

- Costs paid for field emergencies.

- The Summary Insured Rebound option is available.

6.3 What’s Not Included

- Dealing with intentional or self-injury

- The cost of plastic or cosmetic surgery

- Pregnancy treatment, miscarriage, etc.

- Obesity treatment and weight control program

- Treatments Experimental or Unproven

6.4 Eligibility

|

Proposer |

Adult Dependant |

Child/ Children |

|

Min Entry Age: 18 Years |

Minimum Entry Age: 18 Years | Mini Entry Age: 91 Days |

| Max Entry Age: Lifetime Entry | Maximum Entry Age: Lifetime Entry |

Maxi Entry Age: 25 Years |

|

Max Age Entry For Add on Covers |

Maximum Entry Age: 65 Years | Maxi Entry Age: 65 Years |

| Parents & Child Care Cover – Basic & Booster – Entry Age up to 45 Years | Parents & Child Care Cover – Basic & Booster – Entry Age up to 45 Years |

7 Oriental – Individual Mediclaim Policy

Individual Mediclaim Policy of Oriental Insurance is one of the most affordable policies available, which provides cover for medical expenses related to hospitalization and domiciliary hospitalization in case of an illness, accident, or any surgery related to disease which has arisen during the policy period. The sum insured options under the policy range anywhere from Rs. 1 Lakh to Rs. 10 Lakh.

Plan Inclusions and Exclusions

7.1 What’s Included

- Cash compensation for more than 2 days of continuous hospitalization in a regular hospital.

- Hospitalization costs for the patient to remove an organ.

- Charges related to emergencies are secured.

- As a bonus, covering minor injuries.

- Pre-existing diseases, following four continual renewals.

7.2 What’s Not Included

- Aesthetic care, or cosmetic surgery associated costs.

- Circumcision, vaccine, inoculation, without the portion of an illness.

- Surgery for Sight Correction.

- The cost of shows, contact lenses, hearing aids, and so on.

- Any dental or corrective surgery.

7.3 Eligibility

- All Indigenous residents.

- Open to people aged up to 80.

- Until enrolling, candidates over 45 may agree to professional check-ups.

7.4 Tax Benefits

In one year, policyholders can claim tax deductions of up to Rs.25,000 on the premiums. Senior citizens receive deductions of up to 30,000 rs. Such deductions apply under Section 80D of the Income Tax Act, 1961.

8 Raheja QBE – Aarogya Sanjeevani

Raheja QBE Policy Arogya Sanjeevani is a standard product among all health insurance firms. It is suitable for people who are looking for a smaller insured sum, and comprehensive coverage benefits such as hospitalization expense cover, family float cover, modern treatment coverage, and Ayush treatment coverage. The coverage benefits and features of the Aarogya Sanjeevani policy by Raheja QBE are discussed below.

8.1 Plan Inclusions and Exclusions

Not only does the policy provide compensation for injuries and sickness, but it also comes filled with different advantages and services as seen below:

- Raheja QBE provides health insurance business with EMI service.

- The treatment cover for ayushman is provided under the Raheja QBE Aarogya Sanjeevani Scheme.

- The company also pays a 5-50 percent no-payment incentive for failure to lodge a payment within the insurance period.

- All adult and family floaters will purchase the scheme.

- Raheja QBE health insurance company pays even for cataract surgery expenses.

- The program gives a 15-30 day grace period according to payment style.

8.2 Eligibility Criteria for Raheja QBE Aarogya Sanjeevani Policy

The table below mentions who can buy this scheme, age limits, and other parameters:

|

Min Entry Age |

Children – 3 months

Adults – 18 years |

| Max Entry Age |

Children – 25 years Adults – 65 years |

|

Plan Type |

Indemnity |

| Sum Insured (Rs.) |

Rs 1 lakh – Rs 5 lakh |

|

Renewability |

Lifelong |

| Policy Term |

1 Year |

|

Relationships Covered |

Self, spouse, children, parents, and parents-in-law |

| Cumulative Bonus |

5% for each claim-free year 5-50% |

|

Co-payment |

5% |

9 Royal Sundaram Lifeline Supreme Plan

The Royal Sundaram Lifeline Supreme Plan is a comprehensive, individual, and family-friendly health insurance plan. And the premium cost isn’t too much, either. In the same package, that is health policy with the value of a serious condition provision. This covers the most severe safety problems.

This is a flexible program of fitness and wellbeing advantages, Monthly Physical Check-up services, and, among other incentives, Second Clinical Opinion for Serious Illness. If you are over 18 then you can purchase the Royal Sundaram Lifeline Supreme Plan. Then you should apply for a Family Floater package if you choose to involve your partner then children in the same program.

9.1 What is Covered?

Below are the main advantages that the Supreme Lifeline Program provides.

- Hospitalization expenses of hospitalized patients up to Sum Insured.

- Repayment of non- and post-hospitalization costs equal to 60 and 90 days, respectively, of the amount covered.

- All day-care procedures up to the amount insured.

- Cover of an ambulance up to 5,000 rs.

- Coverage up to the total of money covered for the care of organ donors.

- Hospitalization expenses for the home are covered up to the amount insured.

- No-claim bonus (NCB) begins at 20% of the insured amount and extends up to 100%. No NCB reduction, even if a claim is filed during a given year.

- 100% Reload of the insured sum if the insured total and the NCB are completely exhausted.

- AYUSH Treatment — Up to the sum insured in government hospitals and up to Rs. 30,000 in other hospitals, hospital hospitalization cover.

- Animal bite vaccination-Expenses up to Rs 5,000 covered

- Annual safety check-ups for every participant above the age of 18, whatever the argument.

- A second opinion of 11 listed essential diseases for evaluation and care.

9.2 What is Not Covered?

Royal Sundaram would not be resolving lawsuits under the Lifeline Supreme Medical Insurance Program regarding the care of such medical problems. Here is a descriptive description of the program exclusions:

- Pre-existing medical issues as defined in the contract and stated at the point of issuance by the insured would only apply after 36 months of uninterrupted insurance coverage. Any lawsuits would be resolved if there is a delay in program renewal.

- Diseases that the insured person contracts within the first 30 days after the start of the policy will not be considered for claims.

- A serious disease incurred by the covered party during the first 90 days of scheme starting would not be regarded as lawsuits.

- During the first two years of benefits, conditions like Cataract, Benign Prostatic Hypertrophy, Knee / Hip Reconstruction, Chronic Renal Failure / End-Stage Renal Failure, etc. would not be compensated.

9.3 Features and Benefits of Royal Sundaram Lifeline Supreme

|

Eligibility age |

Average age-91 days for addicted children and 18 years for proposer or parent Minimum duration-25 years for addicted children and adult maximum admission period. |

| Policy Type |

Individual or Family Floater |

|

Family Coverage |

Self, partner, and up to 4 dependent children Parents or other dependants may take different float plans. |

|

Policy term |

The option of 1 year, 2 years as well as 3 years |

| Renewability |

Lifetime renewability |

|

Renewal Premium |

The premium payable on renewal based on the age at the time of renewal |

|

Grace Period for Renewal |

30 days from the date of expiry to renew the policy |

|

Sum Insured |

Minimum sum insured – Rs 5 lakhs Maximum sum insured – Rs 50 lakhs |

10 TATA AIG – MediCare

TATA AIG MediCare, a simplified and comprehensive health insurance plan, is designed taking into account the rising costs of medical expenses these days. The scheme protects people in the 5-year age range (dependent children within 91 days and 5 years will only be covered when all parents are covered). The highest enrolment limit is 65 years.

Many of the advantages TATA AIG Medicare provides to its policyholder’s are-regional coverage, lifetime extension, bariatric surgery coverage, and a large network of over 3,000 hospitals throughout India. Beyond this, the insurance provider gives various rate incentives based on the duration of the contract or some level.

Plans Inclusions and Exclusions

10.1 What’s Included

- The organ donor’s medical and surgical expenses on harvesting the organ.

- Daycare procedures during the policy period due to an illness, illness, or injury.

- Post-hospitalization 90 days immediately after the release of the insured citizen.

- 60 days pre-hospitalization immediately before hospitalization of the insured.

- This will be available for in-patient care which is closely linked to hospitalization.

10.2 What’s Not Included

- Obesity treatment, and any program for weight control.

- Treatment is rendered by a physician who is outside his discipline.

- Specific fatigue or exhaustion (“condition to run-down”).

- Psychiatric, mental illnesses (including treatments for mental health).

- Pre-existing diseases are dealt with following a 36 month delay time.

10.3 Features and Benefits of TATA AIG MediCare

|

Features/Plan |

Medicare |

Medicare Premier |

|

Restoration Benefit |

Up to 100% of SI | Up to 100% of SI |

|

No Claim Bonus |

Up to 100% of SI | Up to 100% of SI |

|

Room Rent |

Single private/shared accommodation |

No restriction |

|

ICU Charges |

Actual | Actual |

|

Pre and Post Hospitalization |

60 & 90 days | 60 & 90 days |

11 Manipal Cigna TTK ProHealth Plus

ManipalCigna ‘s policy also addresses your hospitalization, daycare procedures, and home treatments. This provides Medical Care Rewards, Cumulative Premium, Total Insured Recovery, Worldwide Disaster Protection, Health Check-up for Each Renewal, Serious Illness Professional Review, and Complete Protection – up to Rs.1 Crore.

The program pays for any unexpected problems of wellbeing, maternal care, and costs linked to the newborn’s medical services.

Key Inclusions and Exclusions of the Plan

11.1 What’s Included

- An added benefit and available include such as insurance, serious condition, accrued rewards, etc.

- Home care costs are covered up to full Amount Insured.

- The plan provides in-patient care up to the sum insured.

- The Pro-Health health package includes 500 full-day care treatments.

- The plan covers donor expenses, coverage worldwide, maternity, first-year vaccinations for newborns.

- The pre- and post-hospitalization period is 60 and 90 days.

11.2 What’s Not Included

- Dental diagnosis, dentures, dental dentistry, and surgery.

- The study, laboratory devices, and pharmacological regimens.

- Abuse in harmful or hallucinogenic drugs, such as intoxicants and tobacco.

- Insanity, psychiatric diseases, congenital disorders, weight management, and plastic surgery therapies.

- Expenditures for HIV or AIDS treatment and related ailments.

- Implantation/surgery with inherited disease and of stem cells.

11.3 Features and Benefits of Manipal Cigna TTK ProHealth Plus

|

Features/Plan |

ProHealth Protect |

Pro-Health Plus/Preferred/Premier |

|

Restoration Benefit |

Multiple restorations | Multiple restorations |

| No Claim Bonus | Up to 200% of SI |

Up to 200% of SI |

|

Room Rent |

Private single room up to Rs. 5.5 lakh, and any room category above high SI suite | Any room, except suite |

| Pre and Post Hospitalization | Post 90 days |

60 & 180 days |

|

Day Care Procedure |

N/A |

500+ |

12 Universal Sompo – Complete Healthcare Insurance Essential

The Complete Health Insurance Program for Universal Sompo is given to persons and/or the household. The program is intended to cover the hospitalization bills of the covered person(s), as well as the costs of ambulatory care procedures and various value-added facilities.

The affected children may be protected from 91 days up to age 25. This is a framework in which a single policy may protect 13 partnerships.

Plans Inclusions and Exclusions

12.1 What’s Included

- Blood charges, oxygen, are covered.

- It includes expenses incurred on room rental charges, boarding fees, nursing, surgeon/specialist fees.

- Health costs are compensated in case of hospitalization.

- Cashless hospitalization at each of the network hospitals inside the organization.

- Domiciliary hospitalization costs under the scheme are included.

12.2 What’s Not Included

- In the policy’s first year, spending on the care of illnesses such as cataract falls, sinusitis, and associated conditions is not exempted.

- Not covering the pre-existing diseases.

- It is not payable for injury or disease directly or indirectly attributable to war, invasion, the act of the foreign enemy.

- Neither pregnancy nor birth is covered.

- This includes the expense of spectacles, contact lenses, and hearing aids.

12.3 Features and Benefits of Universal Sompo’s Complete Health Insurance plan

|

Key Features |

Highlights |

|

Network Hospitals |

7700+ |

| Incurred Claim Ratio |

104.71 |

|

Renewability |

Lifelong |

| Waiting Period |

4 years |

|

Minimum Age of Entry |

91 days |

| Maximum age of Entry |

70 years |

|

Sum Insured |

3 lakhs, 4 lakhs, 5 lakhs |

| Policy Tenure |

1,2 & 3 years |

|

Premium Calculated based on |

Age, (i.e. sum Insured Chosen) |

13 Kotak General Insurance – Comprehensive Health Insurance Plan

In recent years hospital prices have increased dramatically owing to medical inflation. Every unplanned hospitalization will then burn a hole in your budget and undermine your financial planning. Kotak Mahindra General Insurance Company Ltd. has developed a premium health insurance plan named Kotak Health Premier with this in mind.

It not only covers expenses for consultation fees, medical tests, ambulance fees & hospitalization costs but also rewards you with regular preventive and fitness habits for taking care of your health.

13.1 What’s Included

- Health cost compensation paid on 150 day-care treatments.

- Costs 30 days until hospitalization and 60 days following hospitalization.

- Cumulative 10 percent incentive dependent on regular contract extension amount covered.

- Transport costs incurred up to Rs. 1500 when the insured person is transferred to a hospital for treatment of an illness or injury.

- Health costs accrued over a total and uninterrupted duration of 24 hours during the hospitalization of the covered citizen.

13.2 What’s Not Included

- Sterility, venereal infection, or other sexually transmitted disorder.

- Vaccination or any type of inoculation, unless it is a post animal bite.

- Any costs incurred on the prosthesis, any kind of external durable medical equipment, etc.

- Intentional self-disease and disease or disability induced by the usage, misuse, or misconduct of alcohol or intoxicating substances.

- Routine diagnostic eye or ear test prices, mental dental check-ups, spectacles, and more.

13.3Features and Benefits of Kotak General Insurance – Comprehensive Health Insurance Plan

|

Key Features |

Highlights |

|

Network Hospitals |

4000+ |

|

Incurred Claim Ratio |

48.21 |

|

Renewability |

Lifelong |

| Waiting Period |

4 years |

14 Chola Swasth Parivar Health Insurance Plan

The compensation package includes extensive medical protection on a floating-rate basis for family hospitalization costs as well as specific injury protection for family members on a total amount covered basis.

14.1 Advantages of Chola Swasth Parivar Health Insurance Plan

- Benefits earned under this scheme are for Rs 3 lakhs, Rs. 4 lakhs, and Rs. 5 lakhs Amount Insured. This strategy has two versions-Pearl and Royale.

- Connection to cashless hospitalization services around the region, by impaneled hospitals.

- Spending on pre- and post-hospitalization covered for 30 and 60 days respectively.

- 141 Daycare treatments that do not involve hospitalization remaining 24 hours are provided.

- Domiciliary care is provided if therapy is performed at home in a single insurance year with a period of 7 days.

- Emergency ambulance charges are covered per hospitalization, up to Rs. 2000.

- The organ donor’s treatment expenses at the time of organ transplantation are covered.

- In this policy’s Royal Policy, there is additional insurance where there are floater-based hospitalization compensation and sole treatment of serious injuries.

- Throughout the scheme, there is a lifelong extension.

14.2 Eligibility

- Coverage is provided from age 18 up to age 65.

- From three months on to 26 years, up to two children can be covered if one parent is covered under this plan.

- The program provides provisions for the children themselves, parents and dependents.

- A pre-policy health checkup is only needed after age 55.

14.3 Features and Benefits of Chola Swasth Parivar Health Insurance Plan

|

Basis |

Family floater |

| Sum Assured |

Rs.3, 4 or 5 lakhs |

|

Premiums |

Rs.5,005 to Rs.10,351 |

| Co-payment |

15% compulsory; 10% voluntary (at non-network hospitals) |

|

Coverage |

Inpatient hospitalization expenses: bed fees: 1 percent of the ICU guaranteed amounts chosen: 1.5 percent of the agreed total specified (per day) — Costs of medication for medical staff, consumables, etc. needed for diagnosis — 141-day care treatments — pre / post-hospitalization expenses: up to 30/60 days respectively — daycare services: available in hospitals on the network — Pre-existing diseases |

|

Add-on Covers |

Personal accident cover: Rs.7.5 to 10 lakhs (self) and Rs.3.75 to Rs.5 lakhs (spouse); Rs.1.5 to Rs.2 lakhs (per child) Temporary lifelong disability: Rs.3.75 to Rs.5 lakhs (self) and Rs.1.87 to Rs.2.5 lakhs (spouse); Rs.75,000 to Rs.1 lakhs (per child) |

15 SBI LifeSmart Health Insurance Plan – Arogya Premier Policy

SBI Arogya Premier scheme, a health insurance program launched by SBI in which the insurer/company pays all the medical expenses incurred by the hospitalization/consultation/transplantation. The SBI Arogya Premier Program is intended to compensate medical costs for people and their family members.

Plans Inclusions and Exclusions

15.1 What’s Included

- Coverage of costs for the 142-day care practices.

- Reinstatement of the insured sum up to 100 percent of the insured basic sum.

- 60 days in anticipation of hospitalization and 90 days of post-hospitalization.

- Coverage for real medical costs up to Rs. 1 Lakh for an air ambulance.

- Other treatments covered such as Ayurveda, Unani, Siddha, and Homeopathy.

15.2 What’s Not Included

- Intentional damage to self or violation of the rule.

- Fighting, actions of adversaries from overseas, invasions, conflicts among others.

- Implantation/surgery/storage of the hereditary defects and stem cells.

- Venereal disease, or any disease or illness that is sexually transmitted.

- Treatment with opioid or alcohol, or any product de-addiction.

15.3 Features and Benefits of SBI Arogya Premier policy

|

Minimum age of entry |

18 years for Adults

3 months for children |

| Maximum age of entry |

65 years |

|

Sum Insured |

Rs 10 lakhs to Rs 30 lakhs |

|

Number members can be included |

Under Individual policy: 1 member Under Family Floater: 4 members Family Individual Policy: 5 members |

|

Policy Term |

One Year |

| Premium Paying Modes |

Annually/Monthly |

Factual Representation In Tabular Form

The tabular representation below was provided for a simple and fast comparison of only a few more health insurance policies. The analysis will help you make a smarter choice, so you should finalize which of the proposals best fits your requirements and budget:

|

Health Insurance Plans |

Health Insurance Companies | Incurred Claims Ratio (2018-19) | Maximum Sum Insured Amount | Policy Renewal | Pre Hospitalization | Post Hospitalization | Ambulance Cover |

AYUSH In-patient Treatment |

|

Health Companion Individual |

Max Bupa | 54% | Rs. 1 Crore | Lifelong Renewability | 30 Days | 60 Days | Available up to Rs. 3000 |

Covered |

|

Family Health Optima |

Star Health | 63% | Rs. 25 Lakhs | Lifelong Rewal | 60 Days | 90 Days | Up to Rs. 1,500 per policy period |

Maximum up to Rs. 20,000 as per SI |

|

Optima Restore |

HDFC Ergo Health (formerly known as Apollo Munich) | 62% | Rs. 50 Lakhs | Lifelong Renewability | 60 Days | 180 Days | Up to Rs. 2,000 | Not Mentioned |

| Senior Citizen Red Carpet | Star Health | 63% | Rs. 25 Lakhs | Lifelong Renewability | 30 Days | The plan has specific parameters of calculation explained in detail in the plan brochure | Provided up to Rs. 3,000 |

Not Covered |